Homeownership is one of the best ways to build wealth. According to the U.S. Census Bureau, Americans who own property have a median net wealth nearly 75 times greater than those who rent. However, owning a home is expensive.

Home prices have been rising nationwide, making housing unaffordable in major cities. Despite recent signs of cooling thanks to the Fed’s policy around interest rates, more and more households, especially low- and middle-income households, are struggling to come up with funds to meet the 20% down requirement.

To better understand the financial barriers homebuyers across the country face, we at RealtyHop looked at the years required to save up for a down payment in the top 100 most populated cities in the U.S.

Key Findings

- Los Angeles is the city with the worst barrier to homeownership. It takes 15.74 years for an average family in L.A. to save enough funds and qualify for a conventional loan.

- On the other hand, it takes only 2.25 years for a family in Detroit to afford the 20% down payment on a home, which is around four months shorter than our reporting last year.

- California outranks all other states, with six cities in the top 10, including Los Angeles, Irvine, San Diego, Long Beach, Anaheim, and Santa Ana.

- The barrier to homeownership is generally lower in the Midwest and South. In Chicago, the third most populous U.S. city, it takes 4.73 years for a household to qualify for a mortgage with 20% down. This number is 6.23 years lower than the largest city, New York, and 11.01 years lower than Los Angeles.

The 5 Cities with the Biggest Barrier to Homeownership

1. Los Angeles, CA

With a median list price of $1,200,000, Los Angeles ranks as the city with the most significant barrier to homeownership. Assuming that an average L.A. family set aside 20% of their annual income – $15,249 or $1,271 a month – for the down payment on a home, it will take a whopping 15.74 years of savings for them to meet the loan requirement.

2. Miami, FL

Miami remains one of the most unaffordable cities in the nation this year. The gap between income and home prices worsened in the past few years as out-of-town buyers and investors continued to flock to the city. The median list price has risen to $615,000 in the past year. For local Miami families making a median income of $54,858, it will take 11.21 years to accumulate enough cash for a home.

3. New York, NY

Thanks to rising median household income and decreasing median list price, the barrier to homeownership slightly improved this year in New York City. With a median list price of $839,500 and income of $76,607, it takes homebuyers, on average, 10.96 years to save a 20% down payment for a home.

4. Irvine, CA

Another Californian city made the top five this year. Despite having a considerably high median household income of $122,948 compared to other major cities, it still takes over 10 years for a typical family in Irvine to accumulate enough cash to cover the down payment.

5. Hialeah, FL

Hialeah rounded out our top five this year as one of the cities with the worst barrier to homeownership. With annual savings of $9,906 per year and a median asking price of $480,000, it will take an average Hialeah family 9.69 years to qualify for a loan.

The 5 Cities with the Lowest Barrier to Homeownership

1. Detroit, MI

Detroit continues to rank as the city with the lowest barrier to homeownership in 2024. With a median list price of $85,000, it will take a typical family in Detroit 2.25 years to save up for the down payment if they save 20% of their household income each year.

2. Cleveland, OH

Thanks to relatively low asking prices, homeownership in Cleveland is still attainable for most. With a median home price of $116,250 and a median household income of $37,271, it will take a typical Cleveland family 3.12 years to meet the 20% down payment requirement.

3. Kansas City, MO

The median household income in Kansas City currently sits at $65,256, considerably higher than that of other low-barrier cities included in this index. With a median asking price of $229,500 and an annual savings of $13,051, it will take Kansas City homebuyers 3.52 years to reach the 20% down amount.

4. Milwaukee, WI

In Milwaukee, it takes, on average, 3.62 years for families to save up for a home. In a city where the median list price sits at $179,900, buyers can achieve their goal of homeownership relatively quickly.

5. Wichita, KS

Wichita ties Milwaukee in our rankings this year. With a median household income of $60,712 and a median asking price of $220,000, it takes 3.62 years to accumulate enough cash to cover the 20% down payment required to enter homeownership.

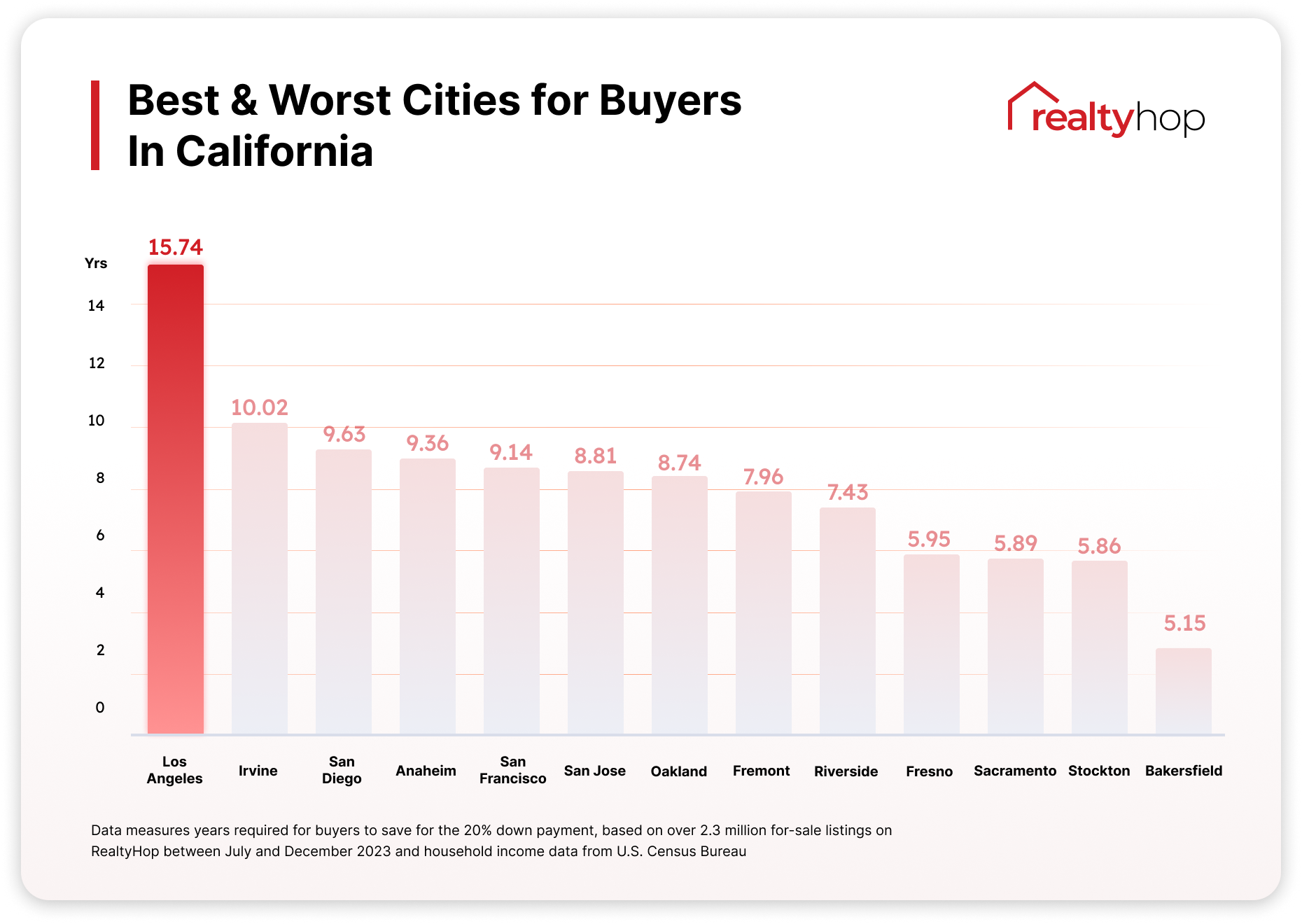

A Closer Look at Homeownership Barriers in California

California remains the most expensive state in America. RealtyHop’s 2023 Most Expensive U.S. Zip Codes study shows that more than half of the 100 most expensive zip codes are in California. While families in certain cities, such as San Francisco and Oakland, have higher incomes, home prices have also been pushed up due to higher living costs and demand.

Of the 18 California cities included in this study, all have a barrier to homeownership over five years. Fremont has one of the highest median household incomes across the country, at $169,023. Despite strong income levels, the barrier to entry remains high at 7.69 years, with a median list price of $1.3 million. Similarly, in Irvine, the median household income currently sits at $122,948, more than double San Bernardino’s. Families there, however, have to spend, on average, 10.02 years to satisfy the down payment requirements.

Full Dataset

Methodology

This report examines the barrier to homeownership across the top 100 U.S. cities by population. We calculated the median list price by city using over 2.3 million residential for-sale listings on RealtyHop between July 2023 and December 2023. To limit the scope of this study and better reflect the prices U.S. households expect to see when buying, the following property types were included when calculating the median: condos, co-ops, single-family homes, and townhouses. Any listings classified as “land” are excluded from this study.

To calculate the years required to save up for the down payment on a home, we first collected the median household income data by city from the most recent ACS data from the U.S. Census Bureau and assumed that a household saves 20% of its annual gross income each year. We then calculated the required years using 20% of the median asking price (down payment) and the amount saved annually.

Tips for Getting a Mortgage

Our research has shown that in major cities in the U.S., especially the most populous ones with job opportunities, owning is not easy. Especially in a high-interest rate environment, buyers looking to enter homeownership soon should plan ahead for financing requirements. Below are a few tips that might help you along the way.

1. Make sure you start saving now

While 20% is generally the requirement to qualify for a loan, the more you put down, the better, as your outstanding principal balance would be lower. This, in turn, brings down your monthly obligation, and less of your money will go toward interest throughout the lifetime of the loan. Any additional cash you’ve saved could also be used to cover some of the closing costs you, as the buyer, have to bear, including the mortgage origination fee.

2. Know your credit score

While you can still get approved even with a credit score of 580 (which is too low for someone who wants to buy a house/apartment), the higher your credit score is, the more likely that you will be approved for a mortgage and enjoy a lower interest rate. Compare rates here and find out if you qualify for a loan.

Keep track of your income, expenses, as well as tax filing documents

If you are self-employed, you are required to submit your tax returns for the previous two years when applying for a loan, and the mortgage lender will take your average income for that period into account to see if you are qualified for a mortgage. It is, therefore, crucial that you keep track of your income and expenses.

3. Choose a mortgage broker

While it might seem straightforward to go with the bank offering you the lowest rate, sometimes lower rates and fees mean poor service and a lack of transparency. Make sure to shop around and fully understand the application process and the mortgage products they offer.

4. Find a First-Time Homebuyer Program

Many states, counties, and cities fund first-time homebuyer programs to help Americans afford the high cost of homeownership. Those looking to purchase property in cities with high barriers to homeownership may consider the following programs:

CalHFA’s MyHome Assistance Program

The MyHome Assistance program provides a deferred payment junior loan of up to 3.5% of the lower appraisal value or purchase price to assist with a down payment and closing costs. This subordinate loan is a deferred payment amount.

There is a cap of $10,000 for all qualified borrowers, and buyers can combine this program with any other grants or down payment assistance programs.

Los Angeles Housing Department Low Income Purchase Assistance

First-time homebuyers in Los Angeles can receive up to $90,000 to cover the down payment, home purchase, and closing costs. Buyers will not have to pay monthly payments but must repay the loan upon the sale, title transfer, first mortgage repayment, or 30 years after receiving the loan.

Miami-Dade Affordable Homeownership Program

Miami-Dade first-time homebuyers can utilize the program to acquire a mortgage loan subsidy as a second or third mortgage with a low interest rate. The program lowers a buyer’s out-of-pocket costs. Participants can only use the program once and must fulfill a 3% down payment, 1% of which must be from their funds.

Miami-Dade Infill Housing Program

The Infill Housing Program caters to Miami-Dade residents who qualify for the Affordable Homeownership Program and aims to increase the amount of available, affordable housing. Infill Developers are currently working to build homes for the program, which applicants must select from when purchasing a home. Homes through the program cannot exceed a sales price of $205,000 or $215,000 if built on a private lot.

New York City HomeFirst Down Payment Assistance Program

Through HomeFirst, qualified homebuyers can receive up to $100,000 for their down payment and closing costs in New York City. The loan will cover all closing costs and half of the down payment. Recipients must purchase a home within the five boroughs to utilize the program.